Reading Meta Platforms as just a social media company is now a serious analytical mistake. But labeling it "the next-generation tech giant transforming into an AI platform" risks letting the narrative run ahead of the evidence. The truth sits between those two poles — and navigating that tension is what separates the well-positioned investor from the one chasing a story.

Step back and four things are simultaneously true: Meta's core advertising machine is one of the most profitable businesses on the planet, delivering $200.97B in revenue and a 41% operating margin in 2025. That same Meta is making a historically large infrastructure bet with a capex guide of $115-135B for 2026 — almost double the prior year. Reality Labs has accumulated roughly $80B in losses since 2020, and added $19.19B more in 2025 alone. And yet, Ray-Ban Meta smart glasses sold more than 7 million units in 2025, tripling year-over-year. Holding all four of those facts in mind simultaneously is the baseline requirement for any serious Meta analysis.

The central question is this: Do these investments and bets constitute a structural new growth cycle that compounds Meta's existing dominance — or are they expensive, uncertain experiments funded by the extraordinary cash generation of the advertising engine underneath? That question drives the valuation, and it drives the positioning of dozens of supply-chain and competitor stocks in Meta's orbit.

What Kind of Company Is Meta, Really?

Meta's monetization engine is simple and almost entirely one-dimensional: it is the most efficient harvester of attention in the digital economy. The Family of Apps segment — Facebook, Instagram, WhatsApp, Messenger, and Threads — generates more than 98% of company revenue through advertising. Roughly 3.58 billion people use these platforms daily; Meta packages that attention and sells it to advertisers. That's the whole model.

The mechanics run deeper, though. Targeted ad delivery is powered by behavioral signals — browsing patterns, social connections, interests, purchase history — that allow Meta to match the right message to the right person at the right moment. The model is self-reinforcing at scale: more users generate more signal, more signal enables better targeting, better targeting commands higher ad prices. Instagram Reels alone generates approximately $50B in annual revenue, and Reels watch time grew 30% year-over-year in 2025 — a growth rate produced not by user count alone but by AI-driven content ranking that keeps users in the feed longer.

Reality Labs — Quest VR headsets, smart glasses, and AR research — represents roughly 1% of consolidated revenue. The segment generated $2.207B in revenue in 2025 against a $19.19B operating loss. That asymmetry can be read as a structural problem or as the cost of a long-duration strategic bet. Which interpretation is correct depends on whether Meta's wearable platform succeeds — a question that won't resolve before 2027 at the earliest.

The right framework for understanding Meta is this: it is an advertising empire. Facebook, Instagram, and WhatsApp each serve distinct demographics and use cases; that diversity dilutes single-platform risk. If a competitor takes a slice of one segment, it doesn't unravel the system. That economic structure gives Meta both the capacity to fund massive AI spending and the financial buffer to absorb regulatory and legal shocks.

AI's Most Immediate Return: Advertising Efficiency

When discussing Meta's AI investments, the headlines gravitate toward Llama models, the Meta AI assistant, and the Superintelligence Labs. Those are long-duration stories. The place where AI is generating measurable, near-term financial return today is advertising optimization — and that distinction matters enormously.

The Advantage+ product family is the clearest evidence. AI-powered campaigns return $4.52 for every $1 of ad spend, roughly 22% higher ROAS than standard campaigns. Facebook AI-optimized ads lifted conversion rates by 5%, Instagram by 3%. Advantage+ usage grew 70% year-over-year in 2025. These percentages look modest in isolation, but applied to a $200B+ revenue base, each incremental efficiency point translates to billions of dollars.

The two-layer framework for AI's role at Meta is analytically useful: Layer One is revenue-generating AI — ad targeting, content ranking, recommendation engines. The return horizon is short, the evidence is measurable, and it's happening right now. Layer Two is long-duration platform AI — Meta AI assistant, Llama models, Superintelligence Labs. The return is uncertain, the timeline is measured in years, and the value depends heavily on narrative.

The content ranking algorithm's role inside this picture is particularly important. Running partly on Meta's own MTIA 300 custom chip, the system determines what appears in a user's feed and what video plays next. As that ranking becomes more accurate, users stay longer. Longer stays mean more ad inventory. More ad inventory means higher Q4 2025 ad revenue — $58.1B, up 24% year-over-year. That is the compounding loop Meta is feeding with AI capital.

Inference: The most reliable near-term ROI from Meta's AI spend is not the frontier model race — it is making the existing advertising machine more efficient. That relationship is both the most defensible and the least disputed value driver.

The Capex Cycle: What Is Meta Actually Buying?

Meta spent $72.2B on capital expenditures in 2025. The 2026 guidance is $115-135B — approaching Google's full-year capex and nearly doubling in a single year. Institutional investors largely read this positively; retail investors skewed skeptical.

The internal composition of that capex matters, because it isn't monolithic. The rough breakdown: approximately 70-80% is AI computing infrastructure — GPU procurement, data center construction, networking, power management, and cooling systems. Roughly 15-20% covers existing social platform infrastructure and server refresh. A small residual goes toward Reality Labs hardware development. The primary purpose of this spend is not superintelligence research — it is scaling inference capacity: delivering Meta AI, ad optimization algorithms, and content ranking at lower per-unit cost to a larger user base.

The financial impact unfolds in three phases. In the 0-12 month window, depreciation load increases and operating margin faces pressure. Meta's operating margin held at 41% in 2025, but net margin declined from 37.9% in 2024 to 30.1% — partly tax-driven, partly rising amortization. As capex roughly doubles in 2026, free cash flow pressure intensifies: the $43.59B FCF generated in 2025 covers less than a third of the new capex target. The gap is absorbed by operating cash flow ($115.8B).

In the 1-3 year window, the payoff phase begins: new data centers come online, inference capacity expands, AI products scale. The Prometheus campus in Ohio (1GW) and Hyperion in Louisiana (scalable to 5GW) are both in active construction. The next-generation MTIA chips — models 400, 450, and 500 — targeting GenAI inference are slated for 2026-2027 deployment, which should reduce per-unit inference cost and ease Nvidia dependence. In the 3-5 year window, the wearable platform sitting on top of this infrastructure could produce the highest-value — and most speculative — returns.

"Is this spend speculative or strategic?" doesn't have a clean answer. But what can be said is that Meta's revenue scale and cash generation remove the short-term existential risk. With $58.74B in long-term debt against an operating cash flow engine of $115.8B, the balance sheet can carry this. The risk is a different one: if the capex output — AI product monetization and wearable platform success — fails to produce visible evidence within 3-4 years, the market's patience will be tested.

Llama, Meta AI, and the Open Model Strategy

650 million downloads is a striking number. Llama 4's launch in April 2025 — Scout, Maverick, and Behemoth variants — expanded the ecosystem. But the investor-relevant question is direct: how does Meta monetize this?

There is no clear direct monetization path right now. Llama does not show up in Meta's revenue line. Instead, it produces three categories of indirect value: it attracts elite AI researchers and engineers, reducing talent acquisition cost at the margin; it generates community contributions that improve model inference efficiency, which Meta feeds back into its own systems; and it creates enterprise lock-in, as businesses that build on Llama gradually deepen their integration with Meta's advertising ecosystem.

Two important constraints bound this strategy, however. With Llama 4, licensing restrictions became more pronounced: platforms with more than 700 million MAUs and certain EU commercial entities now require explicit permission. That erodes the "open source" label — a model cannot simultaneously be strategically constrained and freely open. And in the frontier model race, Meta's technical position remains secondary to OpenAI, Google DeepMind, and Anthropic. The $14.3B Scale AI investment and the creation of Meta Superintelligence Labs represent an attempt to close that gap; the outcome is genuinely uncertain.

Inference: Llama is an ecosystem positioning tool, not a revenue engine. That is worth something — but pricing it into a valuation multiple requires patience that may not be well-anchored in near-term evidence. Meta AI reaching 1 billion active users demonstrates platform scale; the monetization path for those users remains undefined.

The Talent War: Zuckerberg's "List" and the NBA-Level AI Market

By mid-2025, Silicon Valley was witnessing an unprecedented compensation inflation event. Meta's Llama 4 model receiving a cool market reception — combined with OpenAI and Google DeepMind pulling ahead in the frontier race — pushed Zuckerberg into an extraordinary move: the internal creation of a target list known simply as "The List." It named the world's elite AI researchers whom Meta wanted for its new Superintelligence Labs.

The June-July 2025 hiring campaign permanently re-priced the AI talent market. OpenAI CEO Sam Altman publicly disclosed that Meta had offered some researchers $100M signing bonuses. Meta clarified the structure: CTO Andrew Bosworth confirmed that packages near that level exist, but are structured as multi-year stock-and-cash combinations tied to tenure and performance rather than lump-sum payments. The scale, regardless of structure, is real: total four-year packages for elite researchers reached as high as $300M, with some first-year cash realizations reported exceeding $100M.

The names involved illustrate how serious this campaign became. Former Scale AI CEO Alexandr Wang joined as Chief AI Officer through a deal in which Meta acquired a 49% stake in Scale AI at an implied $14.3B valuation. Former GitHub CEO Nat Friedman and former Safe Superintelligence CEO Daniel Gross also joined to co-lead the unit. From OpenAI, researchers Lucas Beyer, Alexander Kolesnikov, Xiaohua Zhai — the Zurich team — and Trapit Bansal (reportedly ~$96M package), who had been central to developing the o-series reasoning models, moved to Meta. Ruoming Pang, who had run Apple's Foundation Models team, joined with a package that exceeded the pay of Apple's most senior executives other than its CEO — Apple declined to counter. Andrew Tulloch, co-founder of Thinking Machines Lab (Mira Murati's startup), initially turned down a Meta package reportedly worth $1.5B, then changed his mind months later.

OpenAI's chief research officer Mark Chen described the departures in an internal memo as feeling like "someone has broken into our home and stolen something" — a measure of how the campaign landed internally at the company being raided. The talent war is bidirectional: Microsoft AI CEO Mustafa Suleyman simultaneously pulled more than 20 researchers from Google. The entire industry entered a recursive loop in which everyone is recruiting from everyone else, continuously re-pricing the market.

For investors, this talent campaign carries two distinct meanings. In the near term, compensation costs are a real operating expense — both the direct package structures and the running cost of staffing Meta Superintelligence Labs. In the medium term, the quality of models these researchers produce determines Llama's frontier positioning. The standard pay scale puts this in context: Meta's senior research scientists earn $305K-$581K in base salary; machine learning engineers reach $440K — before equity, bonuses, or signing packages. Those headline base figures are already 60-80% higher than 2021 levels. What was once a talent premium is now a structural cost of competing in frontier AI.

meta.ai: The Platform Beyond Social Media

Meta's AI product strategy requires evaluating meta.ai as a standalone entity, not just an extension of its apps. The platform represents Meta's most visible effort to distribute its AI assistant across its 3.58 billion users at near-zero marginal distribution cost — a competitive advantage that ChatGPT, Gemini, and Claude structurally cannot replicate, because Meta AI is already present in the apps those users open every day.

Meta AI today operates both as a standalone website (meta.ai) and as an embedded assistant across WhatsApp, Instagram, Facebook, and Messenger. The free tier includes unlimited chat and Q&A, web-style search answers, image generation via Llama-based models, and voice interaction through the standalone app. There is no paywall and no separate authentication required beyond a standard Meta account. The distribution implication is significant: where OpenAI and Anthropic spend on user acquisition, Meta AI distributes by default into 3.58 billion users' existing surfaces.

The feature set has expanded meaningfully. Users can now converse by voice with Meta AI on all major Meta apps, choosing from celebrity-voiced personas including Awkwafina, John Cena, and Judi Dench. Photo analysis and editing are standard — upload an image, ask what's in it, request outfit changes or background replacements, all within the same chat window. Document generation, long-form writing assistance, and code support complete the core assistant layer. The multimodal expansion continues through 2026.

The most strategically interesting — and most debated — product launched on meta.ai is Vibes. Introduced in September 2025, Vibes is a TikTok-style short-form video feed where every piece of content is AI-generated. Users can generate video from scratch using text prompts, work from existing photos or clips, or remix content from others in the feed by layering new music, visual styles, or creative elements. Finished videos can be posted directly to the Vibes feed, shared via DM, or cross-posted to Instagram and Facebook Stories and Reels. For the early launch, Meta partnered with Midjourney and Black Forest Labs for the visual generation layer while its own models continue developing.

Earlier in June 2025, Meta had already shipped a video editing feature across the Meta AI app, the meta.ai website, and the Edits app. The tool allows users to apply more than 50 AI-powered style presets — including vintage comic, anime, space cadet outfit, rainy day lighting, and marble statue effect — to the first 10 seconds of any uploaded video. The integration point is tight: edited videos share directly to Instagram Reels and Facebook Stories, keeping the creation-to-distribution loop inside Meta's ecosystem and reducing creator reliance on third-party editing apps like Capcut or CapCut.

The first user response to Vibes was mixed. The top comment on Zuckerberg's own launch post read "gang nobody wants this," and the majority of visible early reactions were skeptical. That cold start matters — but distinguishing between early-adopter friction and a fundamental product-market fit problem requires more time. Meta's broader pattern with Reels offers a reference point: Reels was received skeptically in 2020-2021 and became a $50B+ revenue segment within three years.

From an investment standpoint, the Vibes strategy is meaningful for a reason that goes beyond the product itself. Rather than competing with TikTok on human-created content — a competition where TikTok's creator density and cultural momentum are genuine advantages — Meta is opening a new lane: AI-generated content where all platforms start from the same baseline. If AI video creation becomes a meaningful user behavior pattern, Meta's existing distribution infrastructure and recommendation algorithms position it to monetize that behavior at scale, converting Vibes content into Reels ad inventory through cross-posting.

Inference: meta.ai's current traffic and monetization numbers are not publicly disclosed. But the platform's structural advantage — near-zero marginal distribution cost into 3.58 billion users — makes it a uniquely positioned AI surface compared to every standalone AI assistant that requires its own user acquisition.

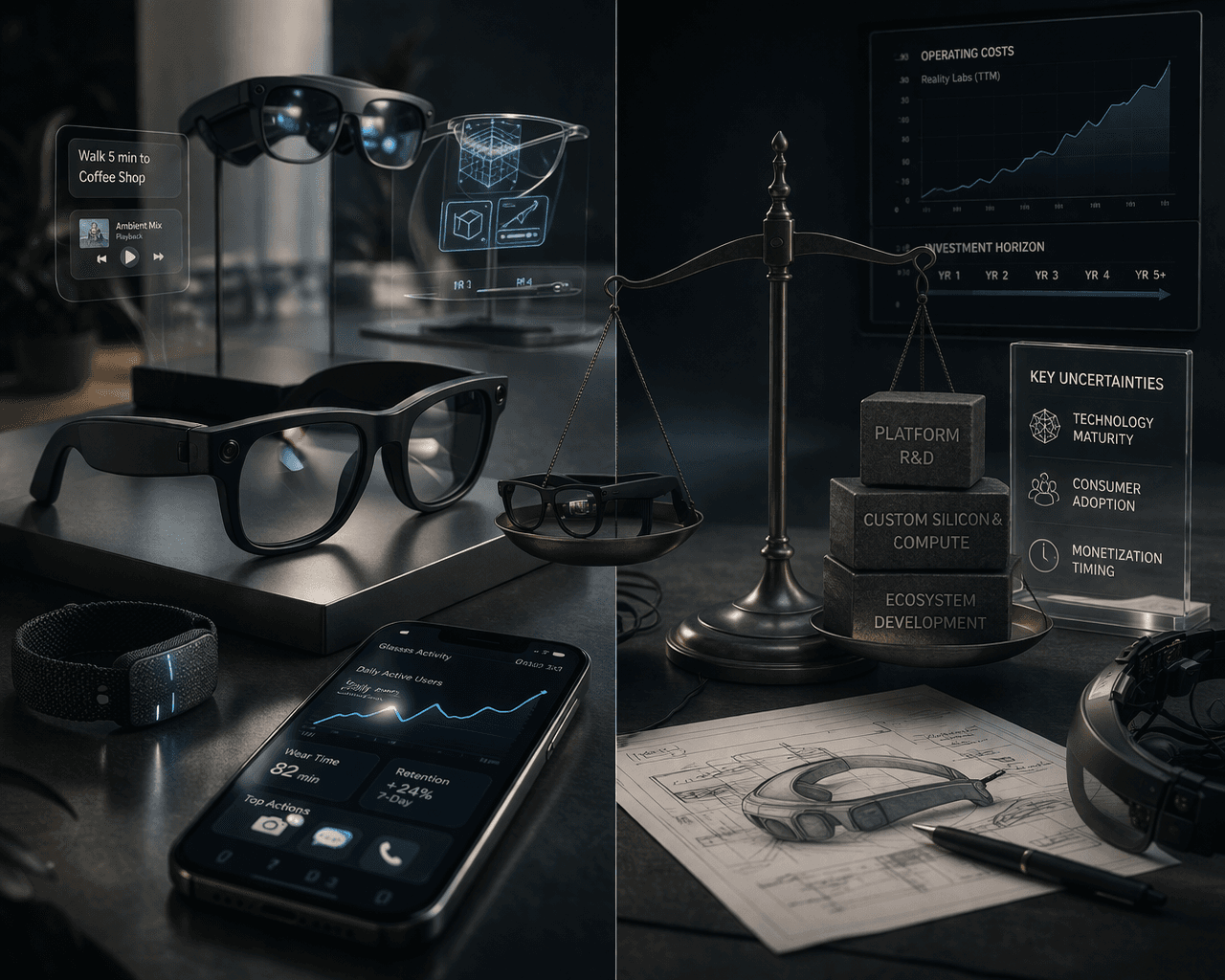

Reality Labs: Loss Center or Real Option?

The blunt read on Reality Labs is easy: roughly $80B in cumulative losses since 2020 against only ~$9B in total revenue. More than 1,000 employees were cut from the division in early 2026. VR headset sales declined in 2025. Zuckerberg's 2021 metaverse pivot has been quietly revised. Ignoring these facts is not analysis.

But the last 18 months of wearable product data tells a different story within that segment. Ray-Ban Meta smart glasses sold more than 1 million units in 2024; in 2025 that number exceeded 7 million — a tripling in a single year. EssilorLuxottica (NYSE: EL), owner of the Ray-Ban and Oakley brands, confirmed in its Q2 2025 earnings that demand was outpacing supply and that it was accelerating production capacity. That is supply chain data, not marketing copy — and it matters because smart glasses have never found mass consumer adoption before.

The product layer needs to be distinguished carefully, though. Ray-Ban Meta today is a speaker, microphone, camera, and AI assistant in a glasses form factor — without any display. It is not AR. The $799 Ray-Ban Meta Display model launched in late 2025 introduces the first limited HUD (heads-up display) element, but is still a partial AR experience. True AR — digital overlays in the real world — lives in the Orion prototype, whose consumer version under the name Artemis is targeting 2027.

Three layers need to be held separately: The VR story (Quest) is weak — the category is growing slowly, and Apple Vision Pro's cold market reception was a sector-wide warning signal. The smart glasses story (Ray-Ban Meta) is real — sales momentum is genuine, category formation is underway, and the platform potential is credible. The true AR glasses story (Artemis/Orion) carries high option value but should not generate meaningful financial estimates before 2027-2028 at the earliest.

Zuckerberg's long-range vision is that when AR glasses displace smartphones, ad delivery, conversion tracking, and personalized assistance on that wearable surface will be more efficient than on a mobile screen. If that scenario materializes, Reality Labs could eventually become Meta's most valuable segment. If it doesn't — or arrives after 2030 — the annual ~$19B loss rate represents destroyed capital. The investor's appropriate posture is to treat this as a real but unpriced option, avoiding both full valuation and total dismissal.

Regulation: Which Risks Are Closed, Which Are Just Getting Started?

The FTC antitrust case — long positioned as an existential threat — closed in November 2025 when Judge James Boasberg ruled that the FTC had failed to prove Meta held monopoly power in personal social networking through its Instagram and WhatsApp acquisitions. The risk of being forced to divest either property was real; it is now off the table. That's a meaningful clearing event.

But the regulatory risks that actually matter for near-term earnings are elsewhere.

EU Digital Markets Act and the ad model: The European Commission ruled in April 2025 that Meta's "consent or pay" model — either share data for ad targeting or pay a subscription fee — violated DMA gatekeeper obligations. Meta committed in March 2026 to offering EU users genuinely less-personalized ad options beginning in 2027. The financial mechanism is direct: if a meaningful portion of European users opts into reduced targeting, Meta's EU ARPU (average revenue per user) declines structurally. With EU revenue representing approximately 20-25% of Meta's total, the erosion is not trivial. Investors who watched the 2021 ATT cycle know this risk well — Apple's privacy update hit Meta hard, and AI partially offset it, but the wound did not fully close.

Child safety litigation — the escalating risk: A New Mexico jury ruled in March 2026 that Meta had failed to take adequate steps to protect minors from sexual exploitation on its platforms, awarding $375M in damages. The same week, a California jury found both Meta and Google negligent in a social media harms trial. Individually, $375M is manageable — roughly one-sixth-hundredth of a quarter's revenue. The significance is precedential.

Thirty-three state attorneys general have filed suits against Meta; the federal multidistrict litigation (MDL) encompasses 2,325+ cases. The trajectory of this litigation depends on how courts interpret algorithmic design liability — specifically, whether the company can be held responsible for harms caused by an algorithm that was deliberately optimized for engagement. If that theory expands legally and Meta is compelled to modify its content ranking systems, the ad inventory growth engine is structurally impaired. That scenario carries far more financial weight than any individual penalty.

Who Benefits From Meta's Spending?

Meta's $115-135B capex cycle is distributing real economic value across a wide range of companies. Understanding that distribution is essential not just for analyzing Meta itself but for positioning in the surrounding supply chain.

Nvidia (NVDA) is the most direct and largest beneficiary. A multi-year, multi-generation strategic partnership now governs the GPU relationship; Blackwell and future Rubin GPU families are flowing into Meta's data centers under this agreement. Meta ranks among Nvidia's largest customers globally. The risk to this relationship is Meta's own MTIA custom chip maturing to the point where Nvidia dependence meaningfully declines.

AMD (AMD) is the most significant new entrant in this supplier ecosystem. A 5-year chip supply deal worth approximately $60B was announced in February 2026, with AMD reportedly receiving a 10% equity option in Meta as part of the structure. That is an extraordinary deal on both dimensions — the dollar scale and the equity alignment put this well beyond a standard vendor contract.

Arista Networks (ANET) is the often-overlooked name. A significant portion of Meta's data center AI networking infrastructure runs on Arista hardware; the Meta-AMD AI collaboration announcement simultaneously confirmed Arista's deeper integration in this cycle. As networking becomes a meaningful bottleneck in AI data centers — not just compute — Arista's strategic position with hyperscalers strengthens.

Broadcom (AVGO) is the most strategically interesting case. Meta is co-developing its MTIA custom chips with Broadcom. The RISC-V-based roadmap targeting inference — MTIA 400, 450, and 500 — is designed to reduce per-token inference cost and reduce Nvidia dependence at scale. The full benefit of this relationship is 3-5 years out, but the multi-generation commitment makes it durable. TSMC (TSM) manufactures these chips; Meta's growing chip orders add directly to TSMC capacity utilization.

In the physical infrastructure layer, Eaton Corp (ETN) and Vertiv (VRT) are positioned at a genuine structural demand inflection. Power management and thermal cooling systems — critical as AI chip thermal loads increase dramatically — have become real capacity constraints in data center builds. Meta's 1-5GW campuses create long-duration demand for both.

EssilorLuxottica (NYSE: EL) sits in a different category entirely: a partner directly capturing the Ray-Ban Meta volume ramp. 7M+ units and supply-constrained demand is already impacting EssilorLuxottica's revenue. The forward risk is a product transition risk: as Meta moves toward true AR glasses, the manufacturing requirements will change substantially, and EssilorLuxottica's centrality in that next phase is less certain than in the current one.

Who Faces Pressure from Meta's Expansion?

"If Meta wins, everyone else loses" is too blunt an instrument. The competitive dynamics are more textured.

Snap (SNAP) is under the most direct pressure. Meta's AI-driven ad superiority makes it progressively easier for advertisers to consolidate budget in Meta's ecosystem, and Snap's ad technology does not operate at a comparable scale. The dynamic is not purely negative — TikTok's continued presence pressures both Meta and Snap simultaneously — but the relative disadvantage widens as Meta's AI optimization compounds.

Pinterest (PINS) is better insulated. Its niche as a "discovery and inspiration" search layer serves a distinct use case that Meta's social engagement model doesn't fully replicate. Meta's commerce-oriented ad products do overlap with Pinterest's territory, but the use-case differentiation provides a meaningful buffer.

TikTok — this competitive read requires a correction from earlier narratives. TikTok's US operations were not banned and did not go away. The Oracle-led consortium (Oracle, Silver Lake, MGX — each at 15%) closed the acquisition of TikTok's US operations on January 22, 2026. ByteDance retains a 19.9% minority stake; US user data and algorithm operations are now under Oracle's oversight. TikTok continues operating for its ~170 million US users. Meta does not capture a windfall from a TikTok exit — the competitor is still there, still growing in creator density and Gen Z retention.

This makes the Vibes strategy more significant as a competitive move. Rather than waiting for TikTok to disappear, Meta is opening a different lane entirely: AI-generated short video where no platform has yet established cultural dominance. The initial user reception was mixed — early top comments on Zuckerberg's launch post ranged from dismissive to hostile — but it is worth noting that Reels also launched into skepticism before becoming Meta's fastest-growing revenue segment.

Alphabet/Google (GOOGL) has a complex bilateral relationship with Meta. On the advertising side, they compete directly for budget; Meta's expanding AI search functionality inside its apps puts marginal pressure on Google's query volume over time. But Meta has also reportedly evaluated Google TPUs for part of its compute stack, creating a potential supplier relationship alongside the competitive one. Google's search moat is deep; the direct earnings impact of Meta's AI expansion on Google is real but limited.

Apple (AAPL) sits at two distinct intersections. On the wearable side, Ray-Ban Meta currently targets a different price tier ($300-500) than Vision Pro — they are not directly competing today. But if the Artemis true AR glasses launch in 2027, a direct product confrontation becomes plausible. On the ad infrastructure side, Apple's ATT policy remains a persistent headwind on Meta's targeting precision; AI has partially compensated for this but has not fully closed the gap.

Microsoft (MSFT) is the most nuanced case. Azure hosts Llama models, making Microsoft a cloud revenue beneficiary of Meta's AI scale-up. Copilot/AI assistant products compete with Meta AI as a productivity surface. In the near term, partnership revenue flows from Microsoft to Meta's ecosystem success; in the longer term, platform competition deepens.

The Counter-Narratives: Meta Is Not Automatically Bullish

Strong analysis generates falsification conditions alongside its thesis. Much of the commentary around Meta falls into the trap of treating upward momentum as a trend line while reducing downside risks to manageable footnotes. That error is avoided here.

AI capex returns may be overstated. The $115-135B guidance is almost three times Meta's 2025 free cash flow. The optimistic case requires: AI model costs continuing to decline, Meta AI users becoming monetizable at scale, and inference demand growing ahead of capacity. If one or two of those assumptions fail, the ROI horizon extends materially. Retail investor skepticism at the capex announcement was not simply uninformed — it reflected a real uncertainty about timing.

The talent war's cost and output are not symmetric. $300M packages for individual researchers are a real operating expense. Whether those researchers produce models that justify the cost depends on technical execution that is not yet visible in published results. Llama 4's cool market reception was the original trigger for this campaign — which means the payoff is still unproven.

Llama's direct monetization path may never become clear. 650M+ downloads is developer engagement, not revenue. The licensing tightening erodes the open-source positioning; the ecosystem advantage only holds if developers continue to choose Meta's stack over OpenAI APIs, Anthropic, or open alternatives.

Reality Labs may continue destroying value for years. The "losses are peaking" narrative has been repeated across multiple earnings cycles. Without a concrete path to profitability, the ~$19B annual loss rate persists. Ray-Ban Meta's momentum is real, but for the division as a whole to reach break-even, the AR glasses category needs to achieve a scale that looks like 2030 at the earliest.

Vibes and AI video faced an authentically cold early reception. User responses to Zuckerberg's own Vibes launch post were largely dismissive. Early rejection is not necessarily fatal — Reels shows that Meta can iterate past a cold start — but product-market fit in AI-generated content is a genuinely open question.

The ad machine is powerful but not recession-proof. 2022 demonstrated this with clarity: a macroeconomic compression combined with the ATT headwind caused Meta's first-ever revenue decline. AI optimization has since produced a V-shaped recovery, but correlation between ad spend and GDP remains high. A macro slowdown would not spare Meta.

Child safety litigation could force platform redesign. Individual verdicts are financially manageable. But if courts expand algorithmic design liability and force modifications to engagement optimization — the core mechanism that powers Meta's ad inventory growth — no AI tool compensates for that structural impairment.

Final Synthesis: Where Is the Value Accumulating?

Recent developments have not weakened the Meta bull thesis — they have resolved several uncertainties while creating new ones. The FTC case closing, Ray-Ban Meta's volume acceleration, ad revenue growing 24% to $58.1B in Q4 2025, and the balance sheet absorbing a capex doubling — that combination represents a strong operational foundation. The New Mexico verdict, the child safety MDL escalation, and the EU DMA compliance trajectory represent genuine new risks. And the talent war's NFL-contract-scale compensation — while signaling frontier AI seriousness — is a cost that will be more fully reflected in 2026-2027 income statements before the research output becomes visible.

What the market is pricing in Meta today can be approximated as follows: the advertising machine's durability and AI's contribution to its efficiency are correctly reflected. Some portion of the wearable platform option is being priced in — the amount of that incorporation is debatable. Reality Labs' chronic loss rate is being largely neutralized against perceived option value. The talent war's cost structure is not yet fully priced.

The question of asymmetric opportunity breaks into three distinct answers. In the core ad-plus-AI-efficiency layer, momentum is strong but the opportunity is largely priced. In the wearable technology option — particularly if Artemis launches successfully in 2027 — there is genuine upside that today's valuation has not fully captured; but it is a speculative bet. In the supply chain layer — AMD's per-unit contribution from the Meta deal, Arista's AI networking revenue, EssilorLuxottica's Ray-Ban Meta volume ramp — there are real, Meta-capex-linked earnings exposures that receive comparatively less attention in mainstream coverage.

Meta today is simultaneously no longer just an advertising company, and not yet a proven new platform leader. The ad machine is strong because AI is feeding it; AI spending and talent acquisition are high because the platform future is uncertain; meta.ai and Vibes are genuine product experiments in democratizing content creation through AI; the wearable option is real because Ray-Ban Meta's sales numbers say so; but that option has not yet converted into measurable financial output. The 2027-2028 window — Artemis launch, Superintelligence Labs' first frontier models, meta.ai monetization model emerging — is when this equation resolves. Until then, the most defensible value layer remains what it has been all along: the advertising machine and the supply chain that serves it.