When we look at Meta today, the real question isn’t whether it’s a strong advertising platform it clearly is. The question is whether Meta is changing its financial identity from a high-margin ad compounder into something closer to an “AI infrastructure builder that happens to own the world’s largest attention graph.” Investors care because those are very different cash-flow profiles: one optimizes for operating leverage, the other willingly trades near-term free cash flow for compute capacity and model advantage.

That tension became much harder to ignore after the January 28, 2026 earnings release (covering Q4 and full-year 2025). Meta delivered a strong finish to 2025, but paired it with a 2026 investment posture that is unusually capital intensive. In other words: the ad engine is healthy, but the company is deliberately choosing a heavier cost-of-growth regime.

How Meta actually makes money

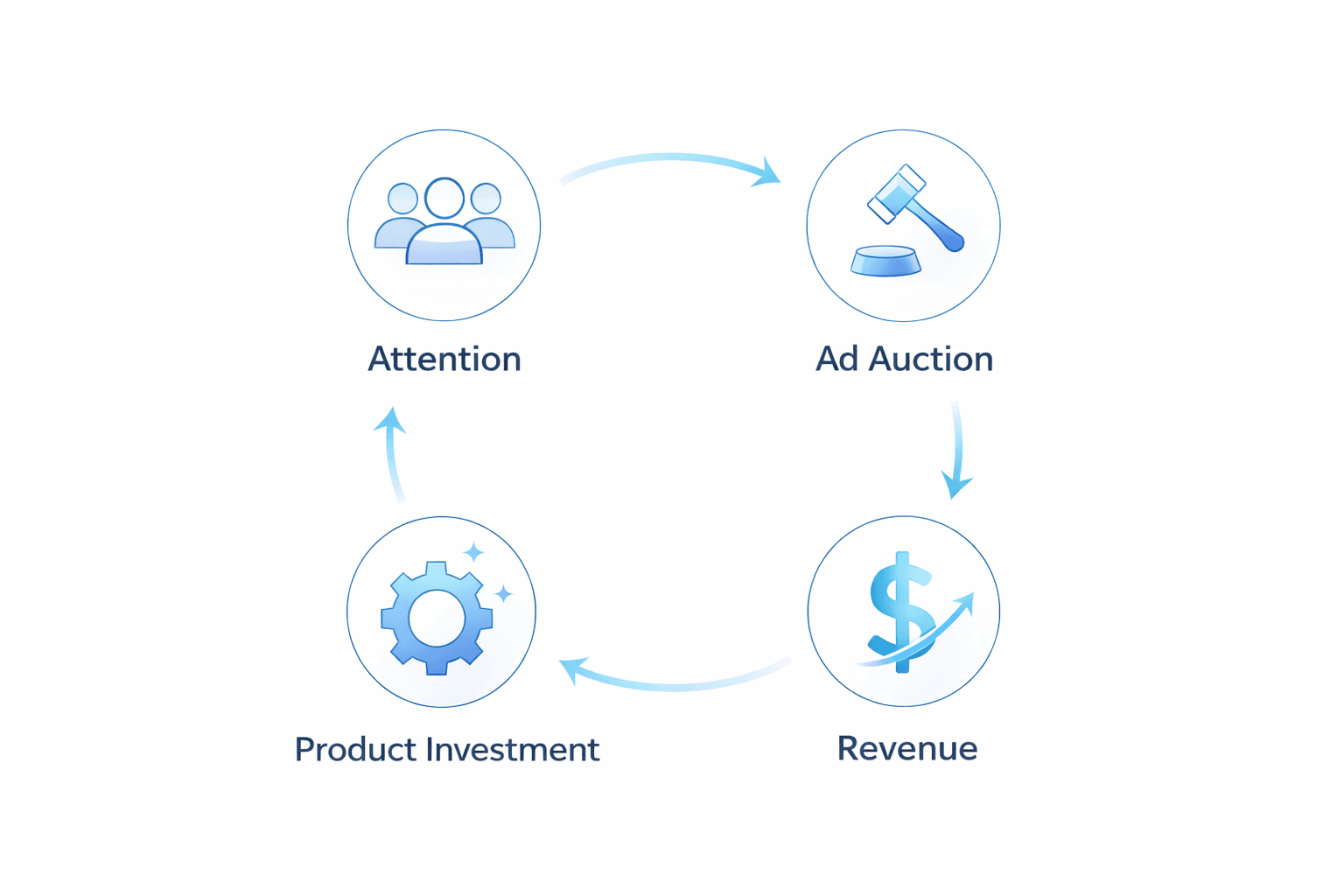

Meta is still, at its core, an advertising business. Full-year 2025 revenue was $200.97B, up 22% year over year, driven primarily by advertising. The underlying mechanics matter: ad impressions grew 12% in 2025 and average price per ad grew 9%. That’s the cleanest signal that the platform isn’t just harvesting more user time; it’s still able to translate attention into higher-value monetization.

The other piece of the income statement that investors can’t hand-wave away is that Meta operates with two economic “worlds” inside one ticker. The core app family throws off substantial profit, while the Reality Labs effort remains meaningfully loss-making, with 2025 Reality Labs operating loss of $19.19B on $2.21B of revenue. This matters less because “metaverse is risky” (everyone knows that) and more because it clarifies what the company must protect: the cash-generation capacity of the ad machine.

Growth drivers: what moves the needle

There are two growth vectors that show up in the numbers and then two that show up in the strategy.

The first is simply scale: Meta reported 3.58B daily active people across its family of apps in Q4 2025, up year over year. At this scale, even incremental improvements in ranking, targeting, and creative optimization can drive meaningful aggregate dollars.

The second is monetization quality especially as consumption shifts toward formats like short-form video. Meta has been clear that different surfaces monetize differently, and bridging those gaps is a multi-year project. The practical point for investors is that “more engagement” isn’t automatically “more profit” unless monetization keeps pace.

Now to the 30/70 weighting you want: AI’s contribution to ad efficiency is real, but it’s not the headline risk. AI improves relevance (for users) and ROI (for advertisers), which tends to support pricing and budget share. But the bigger driver of the equity debate is the investment intensity Meta is choosing to pursue that AI advantage.

The real storyline: AI infrastructure, capex, and the margin/FCF trade-off

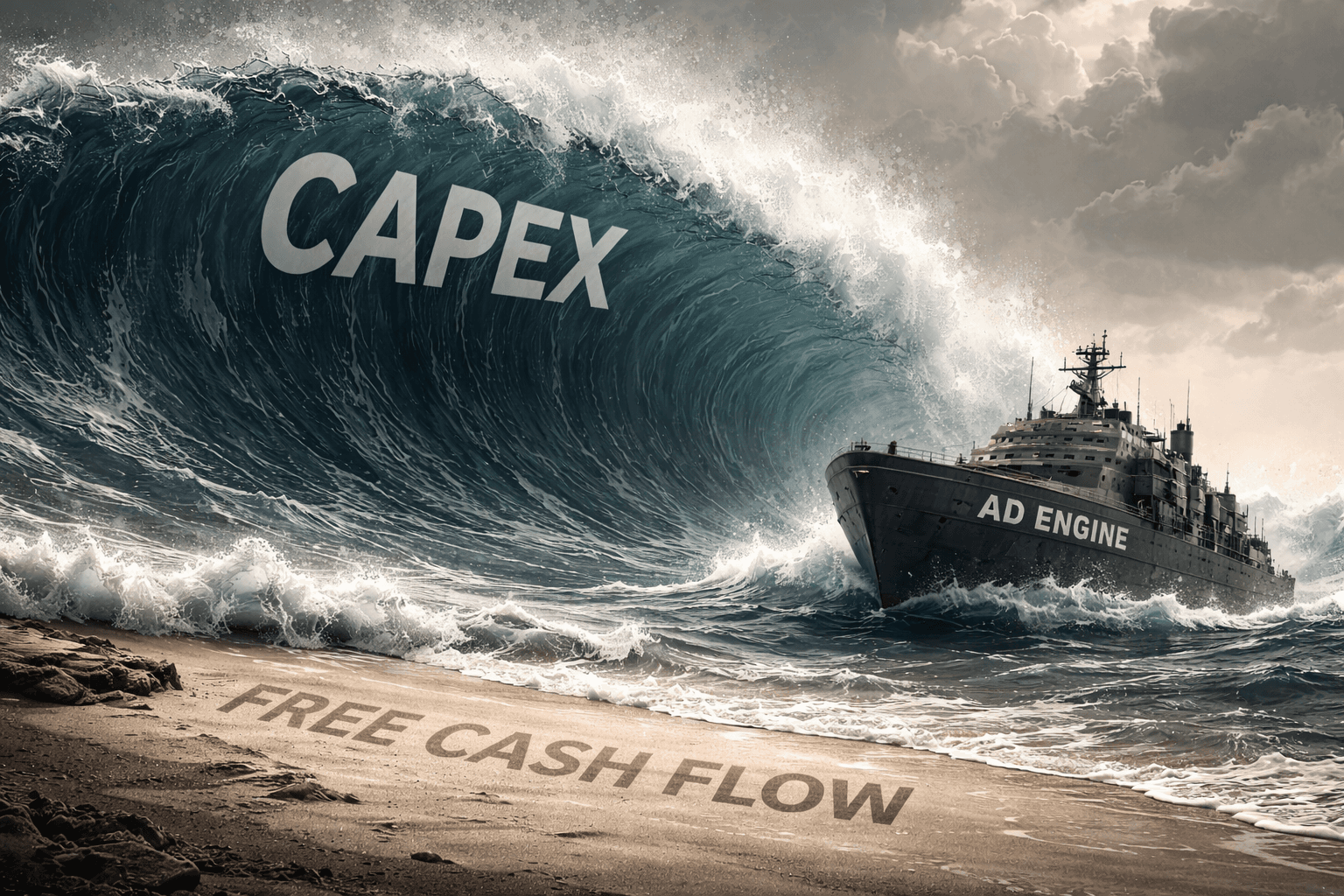

On January 28, Meta guided to 2026 capital expenditures of $115B–$135B (including principal payments on finance leases), a step-up that pulls the conversation away from “will ads grow?” and toward “how long will the company run a very heavy buildout cycle?”

It’s not just capex. Meta also guided to 2026 total expenses of $162B–$169B. The company is explicitly telling you that the near-term operating model is not “maximize leverage,” it’s “fund capacity, fund talent, push the frontier.” That can still be value-creating but it changes what has to go right. In this regime, the stock becomes much more sensitive to (a) whether ad performance holds up while costs surge and (b) whether the investment curve eventually bends down.

Management tried to anchor expectations with a simple line: despite the infrastructure step-up, it expects 2026 operating income above 2025. That’s supportive but the more subtle investor takeaway is this: operating income can look fine while free cash flow gets noisier under a capex wave. If the market starts valuing Meta more on “FCF durability through the buildout” than on “EPS growth this year,” the multiple can behave differently than it did in the leaner period.

Business model risks that actually matter

The risk isn’t “advertising is competitive.” It’s that Meta’s core monetization depends on measurement and targeting working well enough that advertisers keep reallocating budgets toward performance. Any degradation in signal quality or ad effectiveness shows up first as weaker pricing power and then as weaker growth. That’s a structural risk because it hits the engine, not the edges.

The second risk is self-inflicted: if Meta overbuilds capacity relative to realized demand or fails to translate compute into durable product advantage, then the company has chosen a lower-quality cash-flow path without earning the strategic payoff. You don’t need a recession for that to hurt you only need the return on incremental investment to disappoint.

Reality Labs is the third risk, but in a very specific way. The question isn’t whether the segment loses money (it does); it’s whether those losses remain “contained and optional” or start to compete with the AI buildout for resources and investor patience.

Unit economics and operating leverage

The encouraging part is that Meta’s core business still throws off a lot of economic power, and 2025 showed it. Full-year 2025 costs and expenses were $117.69B, while revenue grew 22% that’s the kind of backdrop that allows big strategic spending without immediately breaking the model.

The problem is that 2026 is explicitly set up to test the boundaries of that leverage. Meta can likely “carry” higher cost growth for a while, but investors will increasingly demand evidence that the spend is (1) improving ad outcomes and (2) building a defensible AI platform rather than simply matching the industry’s capex arms race.

Competitive pressure: where it comes from

Meta competes on three fronts that don’t always move together.

First is attention if consumer time shifts, Meta’s inventory mix shifts, and monetization can lag. Second is performance advertising ROI where other ecosystems can win on shopping intent or closed-loop measurement. Third is infrastructure capability where the competitive game looks less like “who has the best ad product this quarter” and more like “who can deliver frontier models at scale.”

This is why a “good product” can still become a tricky stock: the market can love the user-facing AI improvements and still punish the cash-flow volatility needed to fund them.

Sensitivity: small changes that hurt the most

If you want to know what can quietly damage the story, watch a few levers: any deceleration in average price per ad (pricing power) matters more in a high-capex year because it removes the cushion. Expense discipline also matters more than usual because Meta is asking investors to tolerate a step-change in spend; surprises to the upside compound the “FCF quality” worry. And finally, if the monetization gap in newer surfaces doesn’t close, then engagement growth won’t translate cleanly into dollars at the same margin profile.

Scenarios: bear, base, bull

In a bear case, Meta keeps spending at the top end of its capex range while ad pricing momentum softens. Operating income may still be positive, but the market reframes the company as structurally more capital intensive, and the stock stops behaving like a high-leverage ad compounder.

In a base case, the ad engine stays strong enough that Meta can absorb higher expenses and still deliver operating income growth, while investors accept that 2026 is the buildout year and focus on whether 2027 looks more normal.

In a bull case, the investment surge produces visible improvements in ad performance and product utility that translate into sustained pricing power and budget share gains. In that world, capex starts to look less like a drag and more like a moat-building phase the market is willing to finance.

Market reaction

Following the January 28 earnings release, the stock moved sharply higher in after-hours trading (high single digits). The signal is pretty clear: investors were willing to look through the capex shock because the core ad machine printed strong results and the company framed the spend as offensive rather than defensive. The flip side is that this kind of reaction also raises the bar the market is implicitly granting Meta the benefit of the doubt on execution, and that benefit can evaporate quickly if the cash-flow consequences become more visible than the product gains.

Positioning

At this setup, Meta feels long-biased but patience required. The business quality remains high, but the payoff is increasingly tied to whether management can keep ad performance strong while running an unusually heavy investment cycle and then prove that the cycle can taper without losing competitive ground. It’s less about “multiple expansion on optimism” and more about “execution through capex intensity.”

What would invalidate the thesis

If Meta’s ad pricing power weakens meaningfully while the company stays committed to the top end of the 2026 spend envelope, the core “earn through the buildout” narrative breaks.

If AI-driven product improvements do not show up in advertiser outcomes over time meaning the spend looks like matching industry capex rather than generating differentiated ROI the strategic justification collapses.

And if Reality Labs losses or other non-core bets begin to expand in a way that competes with the AI buildout for capital and attention, investors will start treating Meta less like a focused compounder and more like a conglomerate of expensive experiments.

What did the recent developments change? January 28 didn’t change the core thesis that Meta’s ad engine is strong; it changed the frame investors must use. The company is explicitly choosing a more capital-intensive path, so the debate shifts from “how fast can ads grow?” to “can Meta maintain ad strength while underwriting a massive AI buildout and then normalize cash generation on the other side?”